22nd June, 2026

22nd June, 2026

- Why Synthetic Identities Pass Your Current Claimant Verification

- The June 2026 Federal Warning Raises the Cost of Inaction

- How Digital Credentials Verify a Real Claimant Before Payment

- Deploying Claimant Verification Without Replacing Your Benefits System

- How EveryCRED Supports State Workforce Agencies

- Conclusion

- FAQs

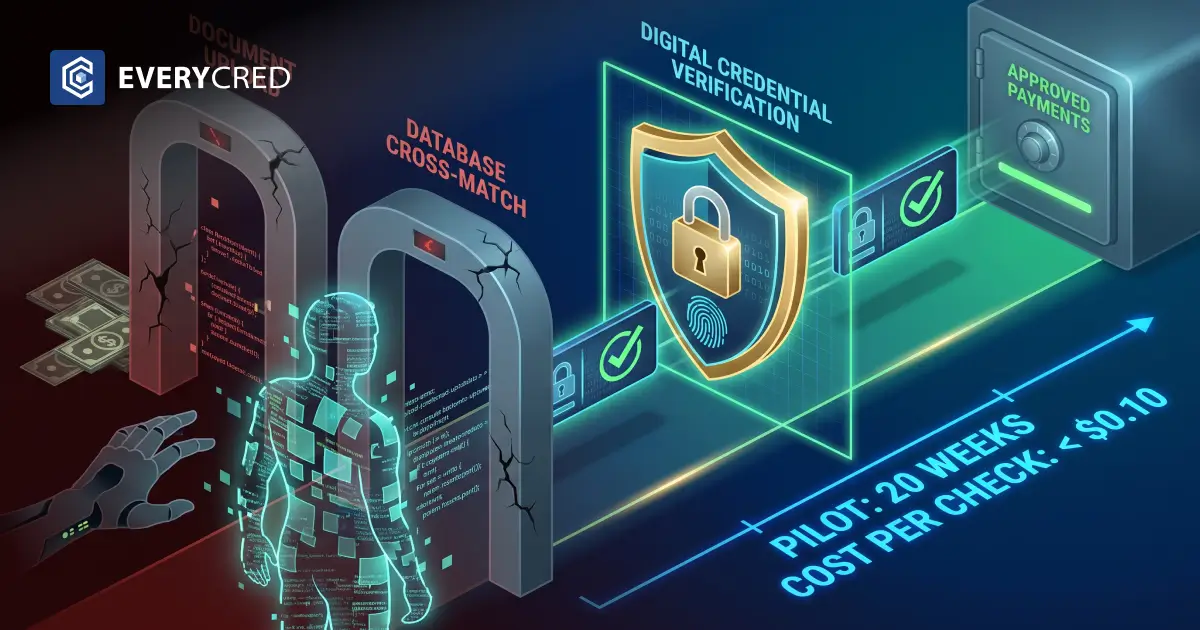

Digital credentials verify a real claimant before a single payment is processed, using a cryptographically signed identity that synthetic identities cannot replicate. This is the gap that document uploads and database cross-matches leave open. A state workforce agency verifies a driver’s license image and Social Security number against a database to confirm that the data exists. It does not confirm that a real, eligible person is behind the claim.

That distinction now carries a federal deadline. In June 2026, state workforce agencies received a warning that administrative funding may be withheld over unemployment insurance fraud losses. Aging benefits systems and weak claimant verification still let synthetic and stolen-identity claims through at scale. This guide explains how digital credentials close that gap, what deployment looks like, and how agencies fund the work without replacing core systems.

Key Takeaways

– Synthetic identities pass document-and-database checks because the underlying data is real; only cryptographic verification confirms a live, eligible claimant.

– GAO reported $186 billion in federal improper payments in FY2025, and AI-forged documents grew 311% from Q1 2024 to Q1 2025.

– Manual verification costs $15 to $25 per check; digital credential verification costs under $0.10 and resolves in seconds.

– State workforce agencies can add claimant verification by REST API without replacing the existing benefits portal, with a pilot operational in roughly 20 weeks.

Why Synthetic Identities Pass Your Current Claimant Verification

A synthetic identity combines real and fabricated data. A fraud operator pairs a valid Social Security number, often stolen from a child or deceased person, with an invented name and address. The result clears most automated checks because each data point resolves against some record.

Current claimant verification relies on two weak steps. The claimant uploads a document image, and the system cross-matches the supplied data against state and federal databases. Both steps are probabilistic. They score how likely the identity is real. They never prove that a specific living person submitted the claim.

AI tools have collapsed the cost of defeating these steps. According to the GAO’s improper payments report, federal improper payments reached $186 billion in FY2025. Forged document quality is rising in parallel. AI-generated fake documents grew 311% from Q1 2024 to Q1 2025, and the entry cost for document fraud is now under $30.

Consider a realistic case. In early 2026, an Eastern state’s benefits portal approved 4,200 claims tied to a single device fingerprint over six weeks. Each claim carried a clean document image and a valid SSN. The agency caught the pattern only after payments cleared, because every individual claimant verification step had passed. Detection scored the risk late. It never verified identity early.

The June 2026 Federal Warning Raises the Cost of Inaction

The federal warning changes the math for every state workforce agency director. Administrative funding is now tied to demonstrable progress against unemployment insurance fraud. Agencies that cannot show a verification upgrade face budget exposure on top of fraud losses.

The cost of the status quo is measurable. Manual identity review costs $15 to $25 per check and adds days to legitimate claims. Synthetic-identity unemployment insurance fraud compounds the cost by paying out claims that should never have entered the queue.

Public-sector teams already use credential-based verification to stop adjacent fraud. The same approach that supports welfare fraud prevention applies directly to unemployment insurance. Identity is the shared failure point across benefit programs.

How Digital Credentials Verify a Real Claimant Before Payment

Digital credentials move identity proof to the front of the claim. Instead of scoring a document after submission, the agency issues a cryptographically signed credential to a claimant at enrollment and verifies it before any payment.

The model uses three roles. The issuer signs the credential, the holder stores it in a wallet, and the verifier confirms the signature. Any alteration to the credential breaks the cryptographic signature and fails verification automatically. A synthetic identity cannot present a credential that a legitimate issuer signed, because issuance requires proofing a real person first.

The economics favor the agency. Each verification costs under $0.10 and resolves in seconds against the issuer’s public key, with no database call or manual review. At 500,000 verifications a year, the first-year savings potential is $7.4 to $12.4 million against manual baselines. Strong identity proofing software at enrollment is what makes the later verification trustworthy.

This approach also meets the standard that agencies are measured against. NIST Special Publication 800-63-4, finalized in July 2025, sets identity assurance requirements that document-and-database checks alone do not satisfy. Cryptographic claimant verification maps to those assurance levels directly.

Deploying Claimant Verification Without Replacing Your Benefits System

State workforce agencies do not need to replace core benefits systems to add this layer. Digital credentials connect to the existing claimant portal through a REST API, the same public sector credentials model used across other benefit programs. The credential check runs before payment authorization, and the claimant-facing interface needs no redesign.

A realistic rollout follows a clear path. The agency issues credentials to claimants during enrollment, the portal calls the verifier before disbursement, and every check is written to an immutable record. Maria, a program integrity officer at a Midwestern agency, framed the goal simply in a 2026 planning session: stop paying synthetic claims at the door, not after the audit.

- Integration: REST API connects to the benefits portal with zero front-end changes.

- Timeline: A statewide build runs about 36 weeks, with a pilot operational by week 20.

- Audit: Every issuance and verification event is logged for federal program-integrity reporting.

- Resilience: Cached signatures allow verification even during portal or network outages.

That audit trail matters under the federal warning. Agencies that deploy audit-ready credentials can prove who was verified, when, and against which credential status, which is exactly the evidence funding reviews demand.

How EveryCRED Supports State Workforce Agencies

We built our claimant verification model on live government deployments, not theory. For Raigad Police, we issued cryptographically signed digital credentials and cut verification time from 30 minutes to under 10 seconds, with an 85% reduction in administrative overhead. The same architecture verifies a claimant before a benefit payment clears.

State workforce agencies can deploy through existing contract vehicles, including NASA SEWP V, ITES-SW2, and NASPO ValuePoint, with no new competitive procurement. Our platform integrates by REST API, logs every event to an immutable audit trail, and meets NIST SP 800-63-4 assurance requirements. Book a demo to see a claimant verification walkthrough built for unemployment insurance.

Conclusion

Synthetic-identity unemployment insurance fraud succeeds because traditional claimant verification proves data exists, not that a real person is eligible. Digital credentials close that gap by verifying a cryptographically signed identity before payment. The June 2026 federal warning makes this upgrade a funding priority, not an option.

The path forward is practical. Agencies add a verification layer by API, keep their existing benefits portal, and run a pilot in roughly 20 weeks. Each check costs under $0.10, resolves in seconds, and produces an audit trail that satisfies federal review. State workforce agencies that adopt digital credentials now stop synthetic claims at the door and protect both their payouts and their administrative funding.

FAQs

How do digital credentials stop synthetic identity unemployment fraud?

They verify a cryptographically signed claimant identity before payment, which a synthetic identity cannot reproduce because issuance requires proofing a real person.

Why do document and database checks fail against synthetic identities?

Synthetic identities use real data points like valid Social Security numbers, so document and database checks confirm the data exists, but never confirm a live claimant.

Can a state workforce agency add claimant verification without replacing its system?

Yes, digital credentials connect to the existing benefits portal by REST API with no front-end changes, and a pilot is typically operational within 20 weeks.

How much does digital credential verification cost per claim?

Each verification costs under $0.10 and resolves in seconds, compared with $15 to $25 for manual identity checks that also add days of delay.

Do digital credentials meet federal identity standards for unemployment programs?

Yes, cryptographic claimant verification maps to NIST SP 800-63-4 identity assurance levels that document-and-database checks alone do not satisfy.